JC Penney gift cards are readily available through gift card resellers for 25% off (or more). This is a nice, easy way to get an automatic 25% savings on all JCP purchases. If you’re willing to order online, though, you can do even better. Currently, the Chase Freedom card offers an extra 10 points per dollar for JCP purchases when you start your shopping within the Ultimate Rewards Mall (just until then end of July). Similarly, ShopAtHome currently offers 10% cash back when you start your JCP shopping within their portal.

With some merchants, points or cashback are not awarded when you pay with gift cards. However, I’ve recently received confirmation that both of the portals I mentioned do work with JCP purchases made with gift cards! Through the Ultimate Rewards Mall, HikerT made 100% of his purchase using gift cards and he used a free shipping coupon code, and he received all of the expected points. Through ShopAtHome, a reader named Steve made most of his purchase with gift cards and small percentage with a credit card. He received the full 10% cash back.

Step by Step

If you’re in the market for JCP stuff, do the following:

- Estimate the total price of all items you plan to buy (including taxes)

- Go to GiftCardGranny.com to find a gift card reseller with cards who’s value add up to the amount you plan to spend. I’ve had good luck buying from both Cardpool and PlasticJungle. I haven’t tried any of the others.

- If buying from Cardpool or PlasticJungle, start at TopCashBack and click through to the appropriate reseller. This will give you 2% to 4% in extra savings!

- Buy the gift cards you need to cover your purchase. If you plan to order online, you may find it easier (and faster) to order e-gift cards. I don’t know whether e-gift cards from JCP can be used in-store.

- When you are ready to make a purchase, log on to either the Ultimate Rewards Mall or ShopAtHome, then click through to JCP.

- Within JCP’s website, pick out what you need and then pay with your gift card(s).

Add it up

With the gift cards, you save 25% off of the total purchase (including taxes!). With the portals, you get back 10% of the pre-tax total. As an example, in a state with 6% sales tax, your tax-included savings would come to 34.4% (or more if you value Ultimate Rewards points higher than 1 cent each). You could save even more if you buy your gift cards after clicking through from TopCashBack.

If you’re in the market for clothes, furniture, housewares, etc. this can be a great way to stack discounts for big savings especially if you find items in which JCP already has a competitive price!

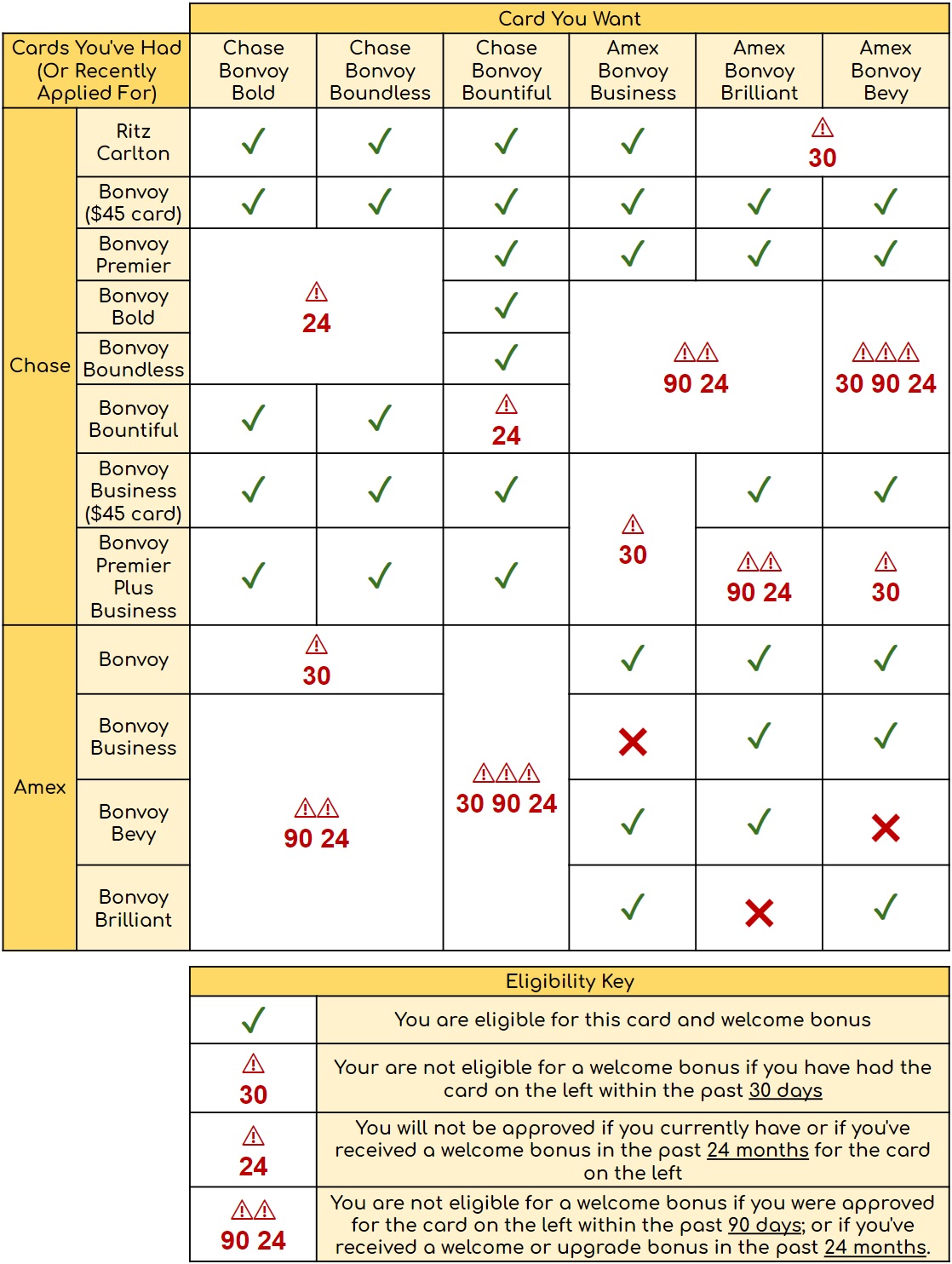

| Chase's 5/24 Rule: With most Chase credit cards, Chase will not approve your application if you have opened 5 or more cards with any bank in the past 24 months. To determine your 5/24 status, see: 3 Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely. |

| Chase 5/24 semantics ("Subject to" vs. "Count towards"): Most Chase cards are subject to the 5/24 rule. That means the rule is enforced in making approval decisions. In other words, you probably won't get approved if your credit report shows that you opened 5 or more cards in the past 24 months. Meanwhile, most business cards (such as those from Chase, Amex, Barclaycard, BOA, Citi, US Bank, and Wells Fargo) are not reported on your personal credit report. These cards do not count towards 5/24. Example: Chase Ink Business Preferred is subject to 5/24, so you likely won't get approved if over 5/24. If you do get approved, it won't count towards 5/24 since it won't appear as an account on your credit report. |

| Amex credit and charge card limits: If you apply for a new Amex credit card, you may get turned down if you already have 5 or more Amex credit cards; or 10 or more Pay Over Time (AKA charge) cards. Both personal and business cards are counted together towards these limits. Authorized user cards are not counted. See also: Which Amex Cards are Charge Cards vs. Credit Cards? |

| Applying for Business Credit Cards Yes, you have a business: In order to sign up for a business credit card, you must have a business. That said, it's common for people to have businesses without realizing it. If you sell items at a yard sale, or on eBay, for example, then you have a business. Similar examples include: consulting, writing (e.g. blog authorship, planning your first novel, etc.), handyman services, owning rental property, renting on airbnb, driving for Uber or Lyft, etc. In any of these cases, your business is considered a Sole Proprietorship unless you form a corporation of some sort. When you apply for a business credit card as a sole proprietor, you can use your own name as your business name, use your own address and phone as the business' address and phone, and your social security number as the business' Tax ID / EIN. Alternatively, you can get a proper Tax ID / EIN from the IRS for free, in about a minute, through this website. Is it OK to use business cards for personal expenses? Anecdotally, almost everyone I know uses business cards for personal expenses. That said, the terms in most business card applications state that you should use the card only for business use. Also, some consumer credit card protections do not apply to business cards. My advice: don't use the card for personal expenses if you're not comfortable doing so. |

| Manufacturing Spend Caution: Many, many things can go wrong when manufacturing spend. If you suddenly increase credit card spend, your accounts may get shut down. If you cycle your balance often (e.g. spend to your limit, pay the bill, repeat) within a billing cycle, your accounts may get shut down. If you repeatedly pay your credit card bill from an anonymous bill payment source, your accounts may get shut down. If you buy lots of gift cards you may lose money due to gift card fraud, theft, loss, or simply mishandling those gift cards (e.g. maybe you thought you already used a gift card and tossed it into your “used” bin). If you rely on only one method to liquidate gift cards, you may be stuck unable to pay your credit card bill when that method gets shut down. In other words, don’t try this at home unless you know what you’re doing, and you understand and accept the risks.. |

| Chase Ultimate Rewards points are super valuable and super flexible. At the most basic level, points can be redeemed for cash or merchandise, but you'll only get one cent per point value that way. A better option is to use points for travel. When points are used to book travel through the Ultimate Rewards portal, points are worth 1.25 cents each with premium cards (Sapphire Preferred or Ink Business Preferred, for example) or 1.5 cents each with the ultra-premium Sapphire Reserve card. Another great option is to transfer points from a premium or ultra-premium card to an airline or hotel program when high value awards are available (see this post for details). If your points are tied to a no-fee "cash back" Ultimate Rewards card, then first move those points to a premium or ultra-premium card before redeeming them in order to get better value. |

| Amex Membership Rewards points can be incredibly valuable if you know how to use them. In general, if you use Membership Rewards points to pay for merchandise or travel, you won't get good value from your points. One exception is with the Business Platinum card where you'll get a 35% point rebate when using points to book certain flights. This gives you approximately 1.5 cents per point value, which is pretty good. Another exception is with the Business Gold Card where you'll get a 25% point rebate when using points to book certain flights. This gives you approximately 1.33 cents per point value. If you don't have either card, then your best bet is to transfer points to airline miles in order to book high value awards. More details can be found here: Amex Membership Rewards Complete Guide. |

| Marriott points can be redeemed for free night awards, travel packages, airline miles, or experiences. 5th Night Free Awards: When redeeming points for free nights, the 5th night within a single reservation is free. Airline miles: Points can be converted to airline miles at a rate of 3 points to 1 mile. With many programs, a bonus is added on when you transfer 60,000 points at a time, such that 60,000 points transfers to 25,000 miles. Also, you'll get a 10% bonus when transferring points to United Airlines. Everything you need to know about Marriott's rewards program, Bonvoy, can be found here: Marriott Bonvoy Complete Guide |

| Editor’s Note: This guest post was written by the same guy who showed you how to fly round trip to Africa (DC to Senegal) for 50,000 points, how to book business class to Europe for 80,000 miles roundtrip, and more. You can find John’s website and award booking service here: theflyingmustache.com/awardbooking. -Greg The Frequent Miler |

Amex Application Tips

Check application status here. |

Chase Application Tips

Call (888) 338-2586 to check your application status |

Citi Application Tips

Check application status here. |

Bank of America Application Tips

Click here to check your application status |

Barclays Application Tips

Consumer: Click here to check your application status |

Capital One Application Tips

To check application status, call (800) 903-9177 or (877) 277-5901 |

Discover Application Tips

Click here to check your application status |

TD Bank Application Tips

Call (888) 561-8861 to check your application status |

US Bank Application Tips

Call (800) 947-1444 to check your application status. |

Wells Fargo Application Tips

Check application status here. |

Under certain circumstances consumer Visa cards don't work with Plastiq. The following payments are fine:

|

In order to meet minimum spend requirements, people often look for options to increase spend in ways that result in getting their money back. These techniques are referred to as "manufacturing spend". American Express has terms in their welcome offers that exclude some manufactured spend techniques from counting towards the minimum spend requirements for the welcome bonus offer. For example, most new cardmember bonuses have terms like this:

Eligible purchases to meet the Threshold Amount do NOT include fees or interest charges, purchases of travelers checks, purchases or reloading of prepaid cards, purchases of gift cards, person-to-person payments, or purchases of other cash equivalents.That said, many techniques for meeting minimum spend are perfectly fine. Here are some techniques that are safe for meeting Amex minimum spend requirements (click each link for more information): |

|

| We have added this to our running list of Black Friday deals, which will be constantly updated through Cyber Monday with a mix of gift card deals, merchandise deals, and travel deals. Check back often. |

Gift Card Granny: Save 2% on Visa eGift cards with promo code LASTMINUTE23 (ends 12/26)")

Gift Card Granny: Profitable 2% Discount On Visa & Mastercard Gift Cards")

Tim: There’s a big difference here. With JCP, you are simply getting points for things that you actually buy. The guys who went to jail were getting cash back without actually buying anything.

Whats the difference between the JCP shopathome rebates and this: http://www.fbi.gov/seattle/press-releases/2012/brothers-who-defrauded-nordstrom-with-online-reward-scheme-sentenced-to-two-years-in-prison-for-wire-fraud. I dont want to go to jail.

Ted F: Both, I believe

When you say can earn points when paying by gift cards, are these gift cards physical ones or electronic? or both?

Have a question for you – a few weeks ago I went to the Ultimate Reward Mall (I have a Sapphire card) and purchased about $500 from Kohl’s. I paid with my AmEx card since I had to spend on it. I never got the Ultimate Reward points. I called up yesterday and the Chase representative told me that in order to get the extra points (10 per $) I needed to use my Sapphire card. So it seems like I am out of luck. How can you then use your JCP gift card to pay and get points from the Ultimate Mall?

Jane

Jane: Usually you’ll get points whether you use a Sapphire card or not to pay. Every now and then, though, there is a blip in which UR mall purchases aren’t recorded properly (regardless of whether you use your Sapphire card). When that happens, it can be difficult to get your points. Call Chase again and ask for your points again. If that doesn’t work, call again. Eventually you’ll get a nice rep who will award you the points.

FM:

Can you explain how using a pre-paid Amex card gets one another 4% off? Tx.

Elle: Read my post “One card to rule them all” for details. The basic idea is this: 1) get a Chase Ink card that gives 5X for office supply purchases; 2) Use Ink card to buy Vanilla Reload cards at Office Depot [you get 5X because it is an office purchase, but there is also a .8% fee on $500 cards, hence 4.2% savings]; 3) load the reload card onto an Amex Prepaid card and use the Amex to pay for things.

Ah. Gotcha. Very helpful. I have the Chase Ink Bold, so I need to try this out.

Thanks for your speedy reply and amazing, helpful posts!

[…] 25% off + 10X UR points or 10% cashback at JC […]

I was about to report the JCP success to you. Yes, I used TopCashBack to buy 30% JCP gift card and used the gift card to purchase some items thru URM along with the free shipping code. All points were posted to my Freedom card yesterday!

FM and Dee Tee:

During the checkout process, if you click “Yes I would like to use a giftcard” it allows you to input two different gift card numbers.

“Enter your gift card information below. You can use up to two gift cards per order”.

FM: I have a 7% utilization when you compare my total combined credit card debt to my total combined spending limits but I have 40% utilization on a singe card. I know the goal is to keep utilization under 30%. Are they referring to a single card or all of it combined? I’m wondering if I should hold off churning until I get my untilization down for that particular credit card? You must get sick of answering the same kind of questions all day. LOL

Joe: that’s a good question and I honestly don’t know the answer. My guess is that you should keep the utilization low within a bank, but again that’s just my guess. I’d recommend asking Frugal Travel Guy since he used to be in the loan business. Let me know what he says!

Steve: Thanks

chuck: Great!

Nevermind – I see this is covered:

http://thepointsguy.com/2012/05/sunday-reader-question-earning-points-through-shopping-portals/

http://www.frugaltravelguy.com/how-to-travel-frugally/online-shopping-portals

Does any one maintain a list of all the different shopping portals?

I know chase has ultimate rewards. Most airlines have one. Citibank has it Thank You portal.

What else? Sometime in the next few months I have my eye on some drapes from pottery barn. It looks like that was once 10X on ultimate rewards from a google search last December.

One more thing, if you buy the GCs with your prepaid Amex, add another 4% to that. This is a very good deal. Do you know if I can combine JCP GC?

Dee Tee: Yep, of course that works to get another 4% or so off just about everything so I don’t bother to mention that often. I don’t know if you can combine JCP gift cards. Anyone else?

Dave: See my post “The best portal finder“.

can you upgrade JCP GCs?

What is your experience with buying the gift cards that are sold on eBay listed on giftcardgranny for significant discount?

Jon: I’ve only bought a few gift cards on EBay. Both took a long time to be shipped (about 6 weeks), but otherwise worked out fine. One advantage is that you get 2% back in EBay bucks.

greek2me: People have reported “no” — you can’t upgrade JCP gift cards.