I currently have 32 active credit cards, 9 prepaid cards, 5 debit/ATM cards, and a constant rotation of gift cards. That’s a problem. It’s not the credit card annual fees that I’m worried about. Many of my credit cards have no annual fee. Others have annual perks that are much more valuable than the fees. And, its not my credit score that’s an issue. I have an excellent score in part because of all of those cards. Almost every time I sign up for new cards, I get extended more credit. This has the effect of making my overall credit utilization ratio lower. And, lower is better.

The problem with having so many cards is knowing what to do with them. I can’t take them all with me wherever I go. Well, I could… but I don’t want to. Plus, I don’t want to increase the chances of all of my cards being stolen or lost. I could lock up all of the cards that I don’t use day to day. But I like to maximize point earnings and take full advantage of credit card perks. When I’m out and about locally, I like to carry cards that offer bonus points at grocery stores, gas stations, office supply stores, and restaurants. At home, I need ready access to cards I’ve chosen for internet spend. When travelling I sometimes need cards that match the airline I’m flying or the hotel where I’m staying. And, I need the cards that get me into airport lounges. When traveling internationally I need to make sure I have cards with no foreign transaction fees and at least one card with a chip just in case I end up somewhere that doesn’t accept credit card swipes.

I have similar problems with prepaid cards and gift cards. Most of the time I don’t need any of them with me, but sometimes I need them when I don’t expect to.

Before I go out shopping or before I go on a trip, I spend a lot of time trying to figure out what should be in my wallet. 90% of the time, I get it right and I have the right cards with me, but sometimes I don’t. Luckily, there is a solution in the works…

Google Wallet isn’t the solution

Last November I reported that Google was planning to launch a credit card that would could be virtually linked to any other credit card you own. The idea would be that you could carry this one Google card around and use your smart phone to select which of your real credit cards it represents at any given time. This card would work as a MasterCard as far as any merchant is concerned, but behind the scenes Google would pass along the charge to whatever card you had selected. See “Google Wallet takes physical form. Are more points in our future?“. Unfortunately, since I wrote that piece, Google axed this project: “Ahead of I/O, Google Wallet Drops Plans to Introduce a Physical Card.”

Walla.by probably isn’t the solution

A company named Walla.by has long teased us with the “One card to rule them all“. The idea is similar to Google Wallet’s idea except even better. The Walla.by card would automatically figure out the best card to use for each situation so as to maximize your rewards everywhere. Cool!

While this solution wouldn’t solve my problem of having too many prepaid cards, gift cards, and ATM cards, it probably would mostly fix my credit card problems. Except that it won’t help when I have to hand over a particular card for some reason (For example, airport lounges will ask to swipe my Amex Platinum card before letting me in). I also doubt it will help when I’ve been targeted for special offers. For example, my US Airways card currently gets 6X in a few categories for a few months. I doubt Walla.by would know about that.

Despite these quibbles, I’d be happy as a clam to get this card (or, maybe I’d be happier than a clam. I’m not really sure that clams are happy. Who came up with that expression anyway?). The problem is that I’m not sure this card will ever really see the light of day. Will the same forces that torpedoed Google Wallet’s physical card cause this one to go down too?

Yes, I’m aware of the irony in the fact that my most popular post ever was titled “One card to rule them all.” I can only hope that Walla.by didn’t trademark the term…

Echo may be just right

Right here in Ann Arbor, Michigan (where I live!), a small company named Protean Payment is developing a new product that could solve all of the issues I listed above. The co-founder of the company, Thiago Olson, used to build fusion reactors in his basement (see “Teen Builds Basement Nuclear Reactor“), but he is now working on something much more impressive: the Echo card. Here’s his mini bio from AngelList:

Protean’s Echo card could be the true “One card to rule them all” because it really can take the place of credit cards, prepaid cards, ATM cards, gift cards, and even loyalty cards.

I met Thiago for lunch last week where we had a great conversation about the Echo card, travel hacking, and the value of points and miles. The Echo card is not yet a real product, but they are hoping to get it out in beta test form in the next four or five months. Luckily for me, they are planning to start their tests in the Ann Arbor area, so I should be able to get in on that early beta test!

As I understand it, the way the card works is as follows:

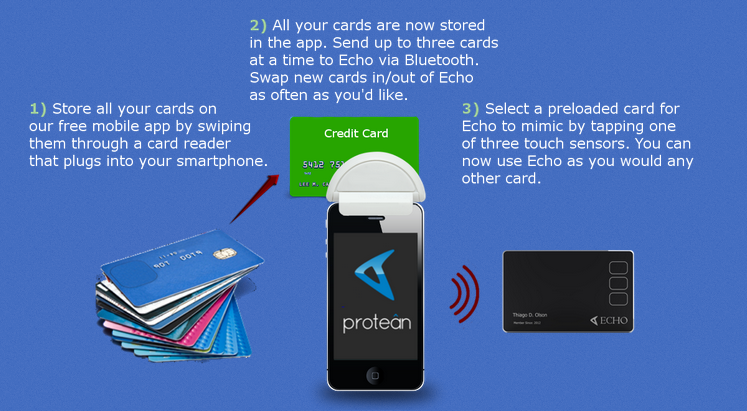

- The user swipes their real credit cards, prepaid cards, ATM cards, gift cards, etc. through a device connected to a smart phone. A smart phone app reads the scanned information and sends it to the Echo card via Bluetooth, where the information is stored in encrypted form.

- On the front of the Echo card are a few touch sensitive buttons that allow the user to select which real card they want to use. When the user selects their desired card, the magnetic stripe on the back is recoded with the exact information that was on the original physical card.

- When the user swipes the Echo card at a register, an ATM, or anywhere else, the Echo card will appear to the card reader to be the original physical card.

You can read more about how the card works here. For security purposes, Echo can be set to lock down when out of range of your phone’s Bluetooth. And, a pin code can be entered directly onto Echo to unlock it for use. Read the card’s FAQ, here.

Interestingly, the picture above which claims that all of your cards are stored on your phone isn’t quite right. Thiago told me that all of the data is actually stored in encrypted form on the card itself (not on your smart phone). The smart phone is simply used to transmit the data to the Echo card, and as an interface to Echo for selecting which card(s) go with which buttons.

The specific mechanism for selecting which card is active is still being decided. There are three physical touch sensitive “buttons” on the Echo card. These can be used to represent three different cards, or they might be used as navigation buttons for scrolling through all of your cards (I would prefer the latter). There will also most likely be a small e-ink display showing which card is currently active.

Not free… yet

When this card initially rolls out, Protean will most likely charge a fee for it. Their website currently states that it will cost between $80 and $100. That said, Protean is hoping that they can work out deals with businesses that would be willing to cover the up front cost of the device in exchange for private labeling or other concessions.

Miscellaneous musings and ideas

- For those who often take a pocketful of Visa gift cards to Walmart (see Gift card PINs) along with their Bluebird and GoBank cards: you should be able to leave those at home once you have this device in your wallet.

- Walla.by and Glyph (which, like Protean, is an Ann Arbor based company) both have apps that help users pick which credit cards to use to maximize rewards. It would be really cool if they would interface with Echo somehow so that the best choice could be sent automatically to the card when needed.

- Thiago pointed out to me that you could load your hotel card key to Echo at most hotels. Not having to carry around a hotel card key would be a nice little perk (but you would have to pack your card swipe device when you travel. I’m not sure I’d go that far).

- Echo doesn’t yet support chip and pin, barcode, NFC or any other RF protocol. So, there are definitely limits to how far you can take it, but I still think it can do 99.9% of what I need (assuming it works!).

- I like the idea of storing loyalty cards to the device, but how often are loyalty cards swiped? Some day Protean might add the ability to display barcodes (using the e-ink display) to cover situations where your card is scanned rather than swiped.

- While the Echo card should work in all automated “swipe” situations, there may be times when a person looks at your card and refuses to swipe it. For example, I could load my Amex Platinum card to the device and try to use it to get into an airport lounge, but I’m not at all sure that it would be accepted since it doesn’t say “Amex Platinum” on the front.

- There are many, many cool things that could be done with this technology, especially once it sports a decent sized e-ink display (text alerts! location aware coupons!…). My hope, though, is that Protean sticks with the fundamentals for now, rather than getting too distracted with the future possibilities. Just get the basics working. I need it!

Thoughts?

I know that I need this card, or something like it. And, yes, I’d be willing to pay up to $100 if it really worked as advertised. What about you? Is this something that you need? How would you use it? Is it worth $80 to $100 to you?

[…] I first wrote about the Stratos Card two and half years ago when it was named Echo. Now, according to The Verge, Stratos has been sold to a smart card company called Ciright One LLC, The Verge reported: […]

[…] past June, in the post “A new card to rule them all,” I wrote about a new credit card device called Echo that could replace all of the cards in […]

[…] could be instantly reprogrammed to mimic any of your credit cards or loyalty cards. FrequentMiler profiles a venture in Ann Arbor that is creating such a product. Sounds nifty, but for $100, I might pass on this […]

Too many security concerns when transferring info from cards to Echo. If someone hacks your phone and the app, all info can be stolen somehow.

Very Interesting article. My wallet is always stuffed full with various credit and gift cards. This is a great concept idea. I wish I had thought of it. I am not so sure about paying for it though. I mean I think it would be worth it, and $100 is not a lot of money, but it just seems like an unnecessary item. But then again it would make life so much easier. I always said getting a smart phone is a waste of money, but now I could not imagine life without it. I have probably 10 different cc’s and many restaurant loyalty cards, beer club cards, AAA cards, business cc, debit card, etc. Having all of that stored on 1 card would be Great! I do fear the risk of my wallet being stolen with this one special card in it that they would be able to access a lot of money. Having some kind of pin to punch to turn the card on and some other security feature would be good. Also, it would be nice to have some sort of money tracking feature on the app.

That’s really funny, since Walla.by is located in MY hometown. I spoke with them late last year — http://hackmytrip.com/2012/12/what-the-wallaby-card-can-mean-for-points-enthusiasts/

[…] it just me or all of you who got excited by Frequent Milers’ latest blog post? “A new card to rule them all“. Reading it was a bit of a step down from the initial excitement envisioning the return of […]

“I have an excellent score in part because of all of those cards. Almost every time I sign up for new cards, I get extended more credit. This has the effect of making my overall credit utilization ratio lower. And, lower is better.”

I assume your logic is : apply more credit cards > Lower utilization ratio > better credit score > be able to apply more credit cards > even better credit score >……

According to your logic, people with 100+ credit cards with have better credit score and the banks are will to approve another 100+ for them. Nice !!!!

@Greg, your comment “I currently have 32 active credit cards, 9 prepaid cards, 5 debit/ATM cards, and a constant rotation of gift cards” reminds me of George’s Exploding Wallet from Seinfeld: http://www.youtube.com/watch?v=yoPf98i8A0g

man, this was a teaser post.. I was so excited. STOP killing us with such posts.

Would be nice to have a tool that you can trust to work 90% of the time.. a manual over ride would be necessary occasionally.

You can always modify the rebate factors periodically. That much work we will always have to do to be part of this game.

I personally doubt someone will pull this off and be profitable. Most people don’t carry more than 3 cards so the market size won’t be large enough

@Paul, that was a cool kickstarter video (http://www.kickstarter.com/projects/1404403369/geode-from-icache) but it seems like the project was never funded and people are trying to get their money from kickstarter/amazon.

Very nifty. It takes someone doing something crazy to push technology forward in an interesting way. For example, look back at mobile phones before the first generation iPhone. They were all terrible. Then that one device forced many companies to innovate. Look forward to the updates on the tests.

Ambitious? Yes.

Do I like it better than Walla.by? Yes

It comes down to execution of course and raising enough dough again.

And I just love to see Ann Arbor startup scene getting more publicity.

There are some really sharp minds living in Ann Arbor, Michigan;-)

For churning, if you can’t manage yourself, you are doing too much. How greedy are you, really?

Hi all – thanks for the questions.

We are preempting concerns related to fraud and card skimming by validating users’ identities prior to allowing payment cards to be loaded their the virtual wallets. The name on cards loaded into the virtual wallet app must (soft)match the validated users’ identity.

How are we validating users’ identities?

A user snaps a picture of their drivers license or passport. We then verify it and run fraud checks on the cloud.

Paul – the last four digits of the card numbers will be available on the application. The card will have a small display so the numbers will be visible on the card itself as well.

Thanks for the feedback guys!

Thiago

Co-founder & CEO Protean Payment